The United States Department of Housing and Urban Development (HUD) has recently revealed plans to lower mortgage insurance premiums (PMI) on Federal Housing Administration (FHA) loans. This adjustment is anticipated to ease and make more cost-effective the process of acquiring homes for Americans with low to moderate incomes.

This substantial PMI reduction means borrowers could save an average of $800 per year on mortgage payments, potentially amounting to thousands of dollars in savings over the loan’s duration. The PMI decrease comes as a result of the FHA’s Mutual Mortgage Insurance Fund’s enhanced financial performance, which has experienced a growth in its capital reserves.

PMI costs can pose a considerable obstacle to homeownership for many Americans, especially those with lower incomes or first-time homebuyers. PMI is mandatory for borrowers who contribute less than 20% down payment on their home purchase and can increase monthly mortgage payments by hundreds of dollars. The PMI reduction is projected to render homeownership more attainable and affordable for such borrowers.

This PMI reduction is part of HUD’s larger initiative to endorse homeownership and widen access to affordable housing. The agency has also initiated the House America Campaign, which seeks to augment the availability of affordable housing, encourage fair housing practices, and bolster economic mobility for low-income families.

Consumer advocates and housing industry groups have largely applauded the PMI reduction, as it is believed to help tackle the ongoing issue of housing affordability in the United States, particularly in costly areas, like Central Oregon, where home prices have dramatically risen in recent years.

The PMI reduction is also predicted to positively influence the overall economy. Homeownership has been demonstrated to contribute to household wealth and foster stronger, more stable communities. By making homeownership more affordable and accessible, HUD aims to spur greater economic growth and stability for all Americans.

It is crucial to note that the PMI reduction is only applicable to FHA loans and does not impact private mortgage insurance (PMI) on conventional loans. Prospective homebuyers should collaborate closely with a lender or housing counselor to comprehend their options and identify the most suitable course of action.

PMI reduction signifies a positive development for low to moderate-income Americans seeking to purchase a home. By cutting mortgage insurance costs, HUD is rendering homeownership more affordable and accessible, which could yield significant advantages for individual households and the wider economy. If you would like to know how this PMI reduction could affect your home-purchasing ability in Bend and surrounding communities, please don’t hesitate to contact us.

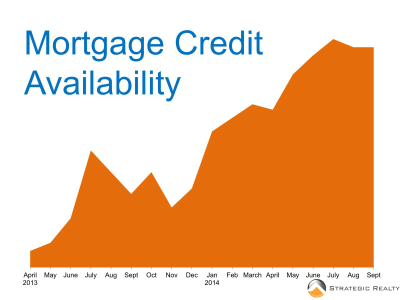

bility of mortgage credit is much higher than in the recent past and it continues to increase. Banks are in the business of loaning money, and as the economy continues to improve they are rapidly focusing on making mortgage loans in this market.

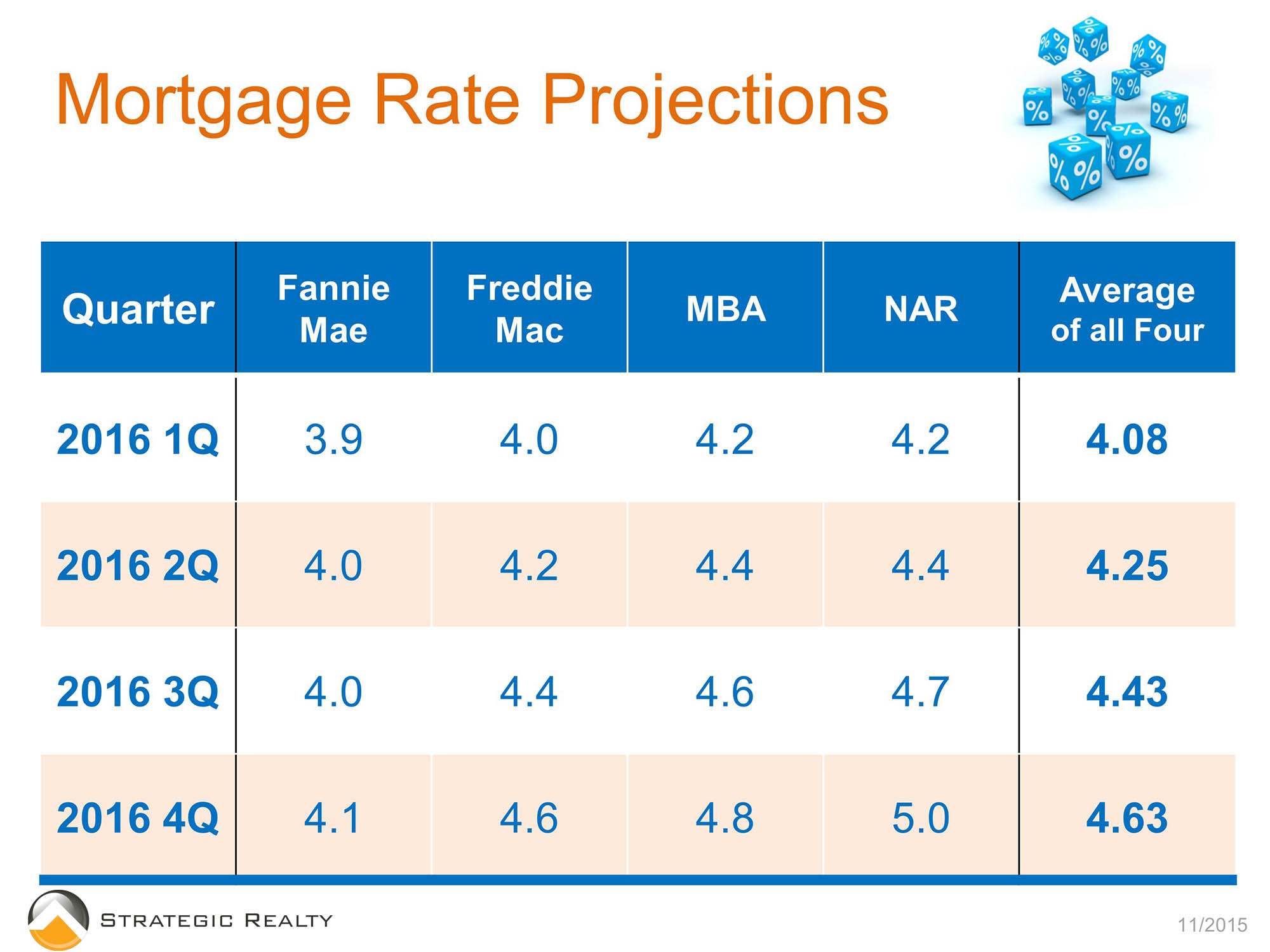

bility of mortgage credit is much higher than in the recent past and it continues to increase. Banks are in the business of loaning money, and as the economy continues to improve they are rapidly focusing on making mortgage loans in this market. ing mortgage rates to continue to increase. Many people look at increasing mortgage rates as just an added expense. What they don’t often think about is that mortgage rate has an incredible impact on the final price of the house you can afford. This is why we are encouraging many of our clients to make their next move now. If you’re thinking about cashing in on some of the equity you’ve made over the last few years, moving up, or going to stay put for several years in your next house, it makes sense to get it done now. Increasing interest rates can not only cost you more money, they can damper the market for selling your home.

ing mortgage rates to continue to increase. Many people look at increasing mortgage rates as just an added expense. What they don’t often think about is that mortgage rate has an incredible impact on the final price of the house you can afford. This is why we are encouraging many of our clients to make their next move now. If you’re thinking about cashing in on some of the equity you’ve made over the last few years, moving up, or going to stay put for several years in your next house, it makes sense to get it done now. Increasing interest rates can not only cost you more money, they can damper the market for selling your home. ng into our office. For a variety of reasons, we feel that finding a mortgage professional you trust is an important second step in any real estate move. Let us know that you would like a recommendation on a mortgage professional and we can provide you with some choices.

ng into our office. For a variety of reasons, we feel that finding a mortgage professional you trust is an important second step in any real estate move. Let us know that you would like a recommendation on a mortgage professional and we can provide you with some choices.